Tax Planning & Consulting

New Law Improves Energy Tax Benefits

Overview: the newly enacted Inflation Reduction Act contains tax credits and depreciation benefits for businesses that implement various types of renewable energy improvements.

Tax Credits Available for Businesses

There are two types of tax credits that are available for businesses which consist of the following:

- Investment Tax Credit (ITC) – The new law increased the ITC from 26% to 30% that are placed in service after 2021, provided that construction commences before 2025. To realize the full tax credit, you must continue to own the property for five years after the energy installation, or the government will recapture some or all of the credit.

- Production Tax Credit (PTC) – is a per kilowatt-hour (kwh) tax credit for electricity generated by solar and other qualifying technologies for the first 10 years of a system’s operation.

Available Stackable "Bonuses" for Tax Credits

In addition to the 30% ITC, starting in 2023 businesses can also utilize stackable “bonus” ITC adders that can increase the ITC up to 50%. The following are the adders:

- Domestic content bonus – You can earn an additional 10% if the project if the steel and iron used is 100% sourced from the U.S. and manufactured components must be at least 40% U.S. sourced. The treasury secretary can provide exceptions to these rules if the cost increases 25% or if not readily available in the U.S.

- · Low-income community bonus – You can earn an additional 10% if the project is located in a low-income community. Low-income communities are those with at least 20% poverty rate or whose residents earn less than 80% of the statewide median income.

- Energy community bonus – You can earn an additional 10% if the project is located in or on a brownfield site or an area with significant employment related to fossil fuels or a coal-related census tract.

The new law provides special depreciation benefits for projects including the following:

- Bonus depreciation – In 2023, the bonus depreciation is 80% which decreases by 20% each subsequent year. Ordinarily, you reduce the basis of the depreciable property by the full amount of the any credit. But the ITC reduces the property’s by only half of the credit amount, increasing your deduction.

- Five-year depreciation – Energy property gets a five-year depreciation under MACRS which is generous because solar panels usually last 25 to 30 years.

Examples of Applying the Tax Credit

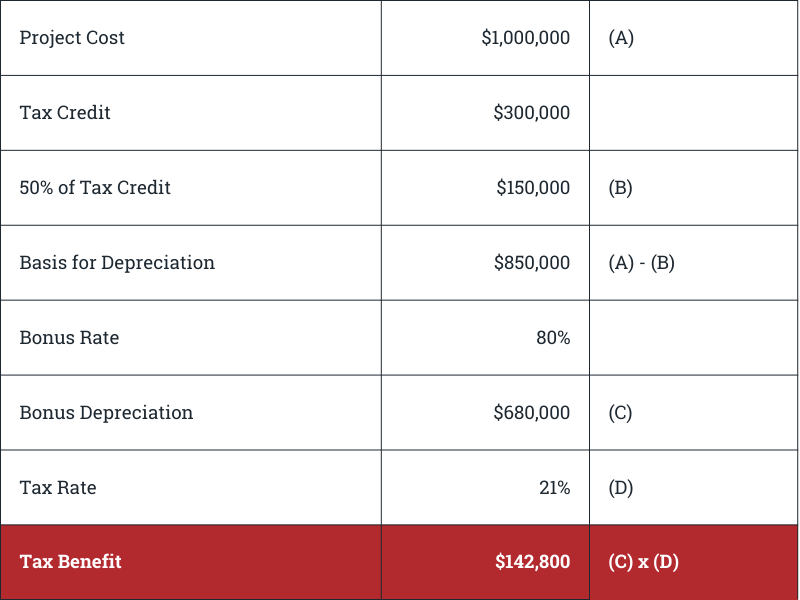

To illustrate how each incentive and the depreciation would be calculated based on a business that commenced construction of an energy project with a cost of $1,000,000 and put in service in 2023:

ITC Calculation:

Step 1: The following represents the tax credit calculation:

Step 2: Once the credit has been calculated, the next step is to calculate the bonus depreciation. Because the business is claiming the ITC, the business gets favorable treatment in the basis. The following represents the bonus depreciation calculation:

Step 3: Once the bonus depreciation has been calculated, the next step is to calculate the depreciation based on 5-year MACRS. The following represents the depreciation calculation:

The following is a recap of the tax benefits for the 1st year of the completed project:

Based on the example, the business had tax benefits in Year 1 of $449,940 on a $1,000,000 project.

The ITC is non-refundable which means it can only reduce your tax liability to 0 and not below. The good news is the ITC is transferable. This allows the business to transfer all or part of your ITC to another taxpayer for cash. The buyer of your ITC need not be a business or be involved in the renewable energy industry but can’t be related to you.

The following is a recap of the ITC:

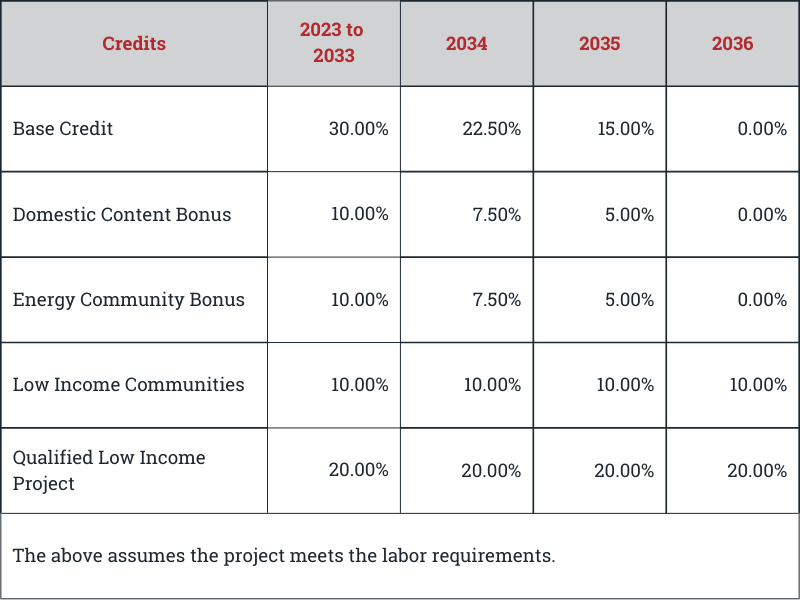

Labor Requirements for the Energy Tax Benefits

To qualify for the full ITC or PTC, projects which commenced construction prior to January 31, 2023, must satisfy the Treasury Department’s labor requirements: all wages for construction, alteration, and repair—for the first five years of the project for the ITC and the first ten years of the project for the PTC—must be paid at the prevailing rates of that location. In addition, a certain percentage of the total construction labor hours for a project must be performed by an apprentice. The percentage increases over time, starting at 10% for projects beginning construction in 2022, 12.5% for projects beginning construction in 2023, and 15% for projects beginning construction after 2023.

Projects can correct the prevailing wage requirements, if they were originally not satisfied, by paying the affected employees the difference in wages plus interest and paying a $5,000 fee to the Labor Department for each impacted individual. The apprenticeship requirements also can be satisfied if a good faith effort was made to comply or if a penalty is paid to the Treasury in the amount of $50/hour of non-compliance. Both penalties increase if the requirements are intentionally disregarded.

Categories

- All

- Auditing(2)

- Business Planning(10)

- CFO Services/Accounting(4)

- City & County Budgeting(1)

- Estate Planning(4)

- Family Planning(1)

- Fiscal Sustainability(7)

- Healthcare(2)

- IRS Representation(2)

- Mergers & Acquisition(1)

- Retirement Planning(14)

- Tax Planning & Consulting(20)

- Utility Rate Study(1)